Separate Trust

A charitable lead annuity trust is a separate taxable trust governed by an irrevocable trust agreement. You choose the trustee who is responsible for administering your lead trust and guiding the investment of its assets.

Irrevocable Gift

A charitable lead annuity trust is an irrevocable arrangement. Once you transfer assets to create the trust, you cannot change your mind and get the assets back. This requirement assures that all of the payments promised in the trust agreement will go to support the University of La Verne.

Make Fixed Payments to the University of La Verne Each Year

Your lead annuity trust makes payments to the University of La Verne each year of a fixed amount for as long as the trust lasts. Your lead trust can make payments to more than one charity, if you wish.

You Choose the Payment Amount

You choose the amount that your lead annuity trust must distribute to the University of La Verne each year. Lead trust donors typically select a payment amount that is likely to preserve a substantial remainder for family or other heirs. Payments are usually made in annual installments, but semiannual or quarterly installments are possible.

Two kinds of lead annuity trusts

A lead annuity trust can pass its remaining assets to your heirs or back to you. These two kinds of lead annuity trust are taxed differently and can help you achieve different philanthropic and financial goals.

The lead annuity trust that passes its remaining assets to your heirs offers a tax-efficient way to make a generous gift to the University of La Verne and provide for your heirs.

The lead annuity trust that passes its remaining assets back to you offers a way to reduce your income tax in the year of your gift and make a generous gift to the University of La Vern over several years, for example to pay off a multi-year pledge.

Learn more below about each kind of lead annuity trust.

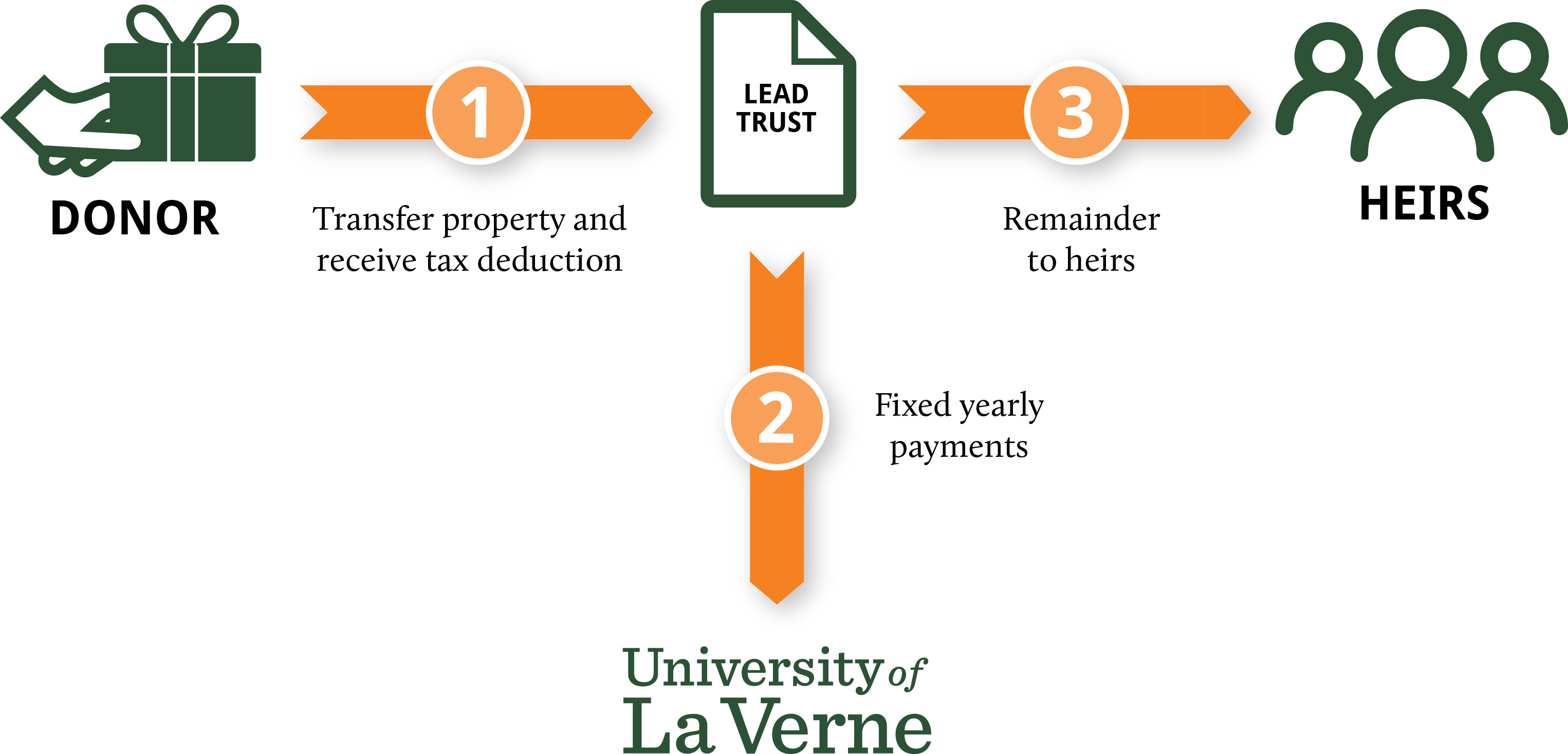

Lead annuity trust that achieves estate planning goals

Remaining Assets to Heirs

When your charitable lead annuity trust ends, all remaining principal in the trust will be transferred to the family members or other heirs you choose.

How Long can my Lead Trust Last?

While most lead annuity trusts last for a specified term of 10-20 years, other terms are possible. Your lead annuity trust can last for one or more lives or for a specific length of time, or for a combination of lives and years. The term length you choose will depend on when you want your heirs to receive their trust distribution and the size of the gift or estate tax charitable deduction you want the trust to generate, as well as other factors.

Tax Benefits

Unlike other charitable trusts, the charitable lead annuity trust generates a gift or estate tax charitable deduction, not an income tax charitable deduction.

- Reduce or eliminate gift or estate tax on gift to heirs if your estate exceeds the then applicable estate tax credit.

- Avoid all gift and estate tax on asset growth.

When you transfer assets to your lead annuity trust, you make a taxable gift to the individuals who will receive your trusts principal when it ends. However, your gift of payments to the University of La Verne earns you a gift or estate tax charitable deduction in the year of your gift that will reduce, and in some cases, eliminate, your taxable gift if your estate exceeds the then applicable estate tax credit.

Some lead annuity trust donors make a point of picking a term length and payout rate that reduces their taxable gift to zero. Doing so eliminates any possibility that they will have to pay gift or estate tax on their gift.

In addition, the assets in your lead annuity trust are removed from your taxable estate. This means that any growth in the value of your trusts assets during its term can be passed on to your heirs completely free of gift and estate taxes.

Taxation of the Trust

A lead annuity trust is a taxable trust. However, a lead trust pays income tax only if its income exceeds the amount it pays to the University of La Verne during the year. A careful trustee can balance your lead annuity trusts income against its charitable payments in order to minimize the income taxes paid by the trust.

Lead Annuity Trusts for Grandchildren

Lead annuity trusts for the benefit of grandchildren present special tax planning challenges related to a tax called the generation skipping tax. For example, you may want to consider creating a charitable lead unitrust in this situation, as it is easier to plan for generation skipping tax issues when creating a lead unitrust than when creating a lead annuity trust. Please be sure to talk to your advisors or to us about these tax considerations

Suitable Funding Assets

You can fund your lead annuity trust with many different kinds of assets. All of the following assets can work well:

- cash

- securities

- a closely-held business

- commercial property

- a combination of these assets

Assets that are likely to increase substantially in value over time can be especially attractive candidates for transfer into a lead trust.

Unlike with many other planned gifts, it can be problematic to fund a lead trust with highly appreciated property. Since a lead trust is fully taxable, selling a highly appreciated asset may cause the trust to owe taxes that will deplete its principal. You will want to work closely with your advisors to pick an asset or combination of assets that will best achieve your goals for your gift.

Willie Soto spent his career building a successful manufacturing business, which he sold a few years ago for $10,000,000. He and his wife, Ann, have three children who are in their 30s. Willie has been reviewing his estate plan with an eye toward adding a major gift to the University of La Verne. Funding a charitable lead annuity trust offers an excellent way for Willie to provide generous support to the University of La Verne and pass assets to his three children. Willie chooses to create a $2,000,000 lead annuity trust that will pay $130,000 to the University of La Verne each year for 20 years.

Benefits

- The Sotos' three children will split approximately $2,409,955* when the trust ends.

- The Sotos will earn a gift tax charitable deduction of $1,592,962**.

- The assets used to fund the trust will not be taxable in their estate.

- The University of La Verne will receive $2,600,000 from the trust over 20 years.

* Assumes the trust assets earn a 7% annual net return.

** The Sotos' estate or gift tax charitable deduction may vary depending on the timing of their gift.

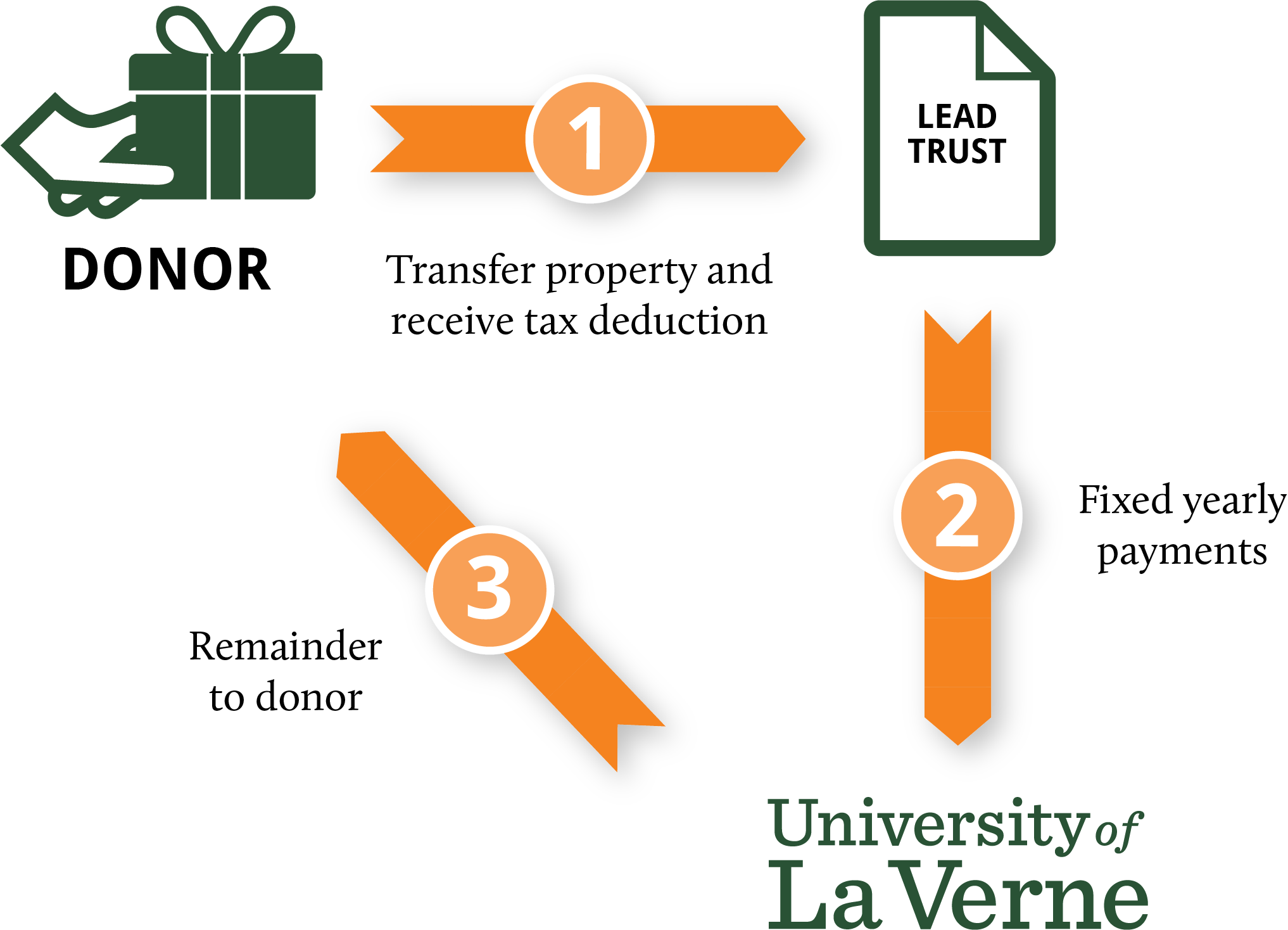

Lead annuity trust that achieves income tax planning goals

Remaining assets return to you

When your charitable lead annuity trust ends, all remaining principal in the trust will be transferred back to you.

How long can my lead trust last?

Most lead annuity trusts that return their remainder to the donor last for a specified term of 5-10 years, although some donors choose a longer term. The term length you choose will depend on when you want to get back the assets remaining in the trust and the size of the income tax charitable deduction you want the trust to generate, as well as other factors.

Tax benefits

The charitable lead annuity trust generates an income tax charitable deduction for you in the year of your gift. The longer your trust’s term and the larger its payments to the University of La Verne, the bigger your deduction will be.

The amount of your deduction that you can take each year generally is limited to 30% of your adjusted gross income. If you are unable to use all your deduction in the year of your gift, you can carry forward your unused deduction up to five additional years.

Taxation of the trust

All income earned by the lead annuity trust during its term is reported on your personal income tax return and taxed to you. You do not get a charitable deduction for the trust’s payment to the University of La Verne each year because you already received a charitable deduction for all these payments in the year you created the lead trust.

Common reasons to create this kind of lead annuity trust

Donors create a lead annuity trust that returns its remaining assets to them for many reasons. Two common ones are:

- To earn a large deduction to reduce income tax in a year of unusually high income, such as after selling a business or receiving a large bonus.

- To pay off a multi-year pledge in a tax-advantageous way.

Suitable funding assets

This kind of lead annuity trust is usually funded with cash or securities. Income earned by the trust, including realized capital gain, is taxable to you. You will want to work closely with your advisors to pick an asset or combination of assets that will best achieve your goals for your gift.

Example

Miriam Froman has been a generous supporter of the University of La Verne for many years. She would like to create an endowed scholarship fund, which requires a gift of $500,000. She chooses to fully fund her scholarship over five years by creating a 5-year $500,000 charitable lead annuity trust that will pay $100,000/year to the University of La Verne.

Benefits

- Miriam will receive an income tax charitable deduction of over $480,000*.

- Over five years, Miriam will endow a $500,000 scholarship fund at the University.

- The lead trust will return over $125,000 to Miriam when it ends**.

- * Miriam’s income tax charitable deduction may vary depending on the timing of her gift.

** Assumes the trust assets earn a 7% annual net return.